When Should I Start Learning My Medicare Options?This is a question we hear all the time from people who are close to age 65. Medicare is complicated, and how and when you enroll will depend on your unique situation: whether you will continue working once you are on Medicare, what, if any, group health insurance might be available to you, whether you are going to start taking Social Security at age 65, and the list goes on. In this video, we’ll discuss the ideal, realistic timeline to get you prepared for Medicare with the least amount of stress and confusion possible. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

Most Important Advice

Here’s the most important thing: don’t wait until the last minute when it comes to enrolling in Medicare itself. By that, I mean Medicare Parts A and B. You can apply for Medicare Parts A and B online at https://www.ssa.gov/benefits/medicare. You can also call Social Security or visit your local Social Security office to apply for Medicare. For many people, applying any of those ways goes fairly smoothly and a Medicare ID number is assigned and a Medicare card arrives in the mail within about 30 days. However, sometimes the enrollment process does not go smoothly at all. Clients have had significant delays applying for Medicare using all three of those enrollment options. If you can’t log into the Social Security website, a card with an activation code will be mailed to you if you request one. In about 10 days. Both the phone centers and local offices in some places have been experiencing long wait times for appointments due to staffing shortages and the pandemic. Because having a Medicare ID number is the first necessary step before enrolling in any other Medicare coverage, if you wait until the last month before you want your coverage to start and run into any trouble with Social Security Medicare enrollment, there’s a good chance you won’t have everything completed when you’d like. So, if a month isn’t enough time, when should you start? The ideal time to start learning about how Medicare works, what your coverage options are, and when you should enroll in what, is three to six months before your Medicare eligibility begins. This isn’t to say that all your time should be spent learning about Medicare. That could drive you insane. By starting early, you can avoid potential Social Security office delays and break your Medicare learning into small chunks. We have a simple checklist to follow that can help. Enrollment Rules Although all the enrollment rules for Medicare and Medicare plans are publicly available, Medicare doesn’t guide you through all of them or give you specific instructions tailored to your particular situation. For most people, the most important time for making decisions about Medicare coverage is the 7 month period around your 65th birthday. The three months before your birth month, your birth month, and the three months afterward are your Initial Enrollment Period. If you want your Medicare coverage to start on the first day of your birth month, you have to apply before your birth month. That’s the government side of things. Individual Medicare Plans Medicare was never intended to cover all of your medical expenses. Because of that, most people also enroll in Medicare coverage beyond Medicare Parts A and B. By that, I mean Medicare Supplements, Medicare Advantage plans, and Medicare Part D plans. All of these are offered through private insurance companies. Medicare has rules governing when and how you can enroll in each of these plans too. The rules are not the same for every type of plan. Medicare Supplement vs Medicare Advantage With a few exceptions, the two major routes a person can take for individual Medicare plans are either a Medicare Advantage plan or a Medicare Supplement plus a standalone Part D prescription drug plan. To be able to decide which route is best for you, you have to take a look at what is available where you live and what type of plan fits your medical and financial situation best. This video explains the differences between Medicare Advantage plans and Medicare Supplements in more detail. Once you’ve decided which type of plan is right for you, you can start comparison shopping all the insurance companies that offer that type of plan in your zip code. Then, in the future, if you are covered by a Medicare Supplement, you can comparison shop again every time rates change. Or if you are in a Medicare Advantage or Part D plan, you can comparison shop every year during the Annual Enrollment Period. Internet Caution You can do all this on your own, but you don’t have to. And really, I don’t recommend that you do. The great thing about the internet is that anyone can put content here.... The bad thing about the internet is that anyone can put content here.... A lot of our time on the phone is spent debunking incorrect information that people found doing internet research into Medicare plans. Plenty of people who are successful in their fields of specialty have gotten themselves into real tight spots with Medicare by relying on information they found on the internet that was misleading or flat out wrong. If you see something online that claims to be a way to get around late enrollment penalties or income related monthly adjustment amounts or anything “secret” about Medicare that “they” don’t want you to know, it’s likely not correct. Any statement online made about Medicare or Medicare plans should be verifiable on medicare.gov or your state health insurance department website. If a Medicare plan broker can’t back up what he or she is telling you with documentation, look for another broker. Free Help is Available Honest, reputable brokers are here to help you every step of the way from learning about your options and answering your questions to enrolling in Medicare itself and Medicare plans and changing or renewing those plans in the future. We do this all at no cost to you. If you enroll through our office into a plan offered by any of the many insurance companies we contract with, we receive a commission for your enrollment. Because the commissions for Medicare plans are about the same regardless of which plan or company you choose, we can be impartial when comparison shopping plans and put your best interest first. The price is the same for you whether you purchase a Medicare plan by yourself direct from an insurance company or you purchase through our office, so why not take the extra free assistance? If you have questions about Medicare coverage, please feel free to give our office a call at 877-312-1414 or schedule a free, no obligation Medicare Plan Consultation. We’re here to help take the confusion out of Medicare and Medicare plan enrollment and find the best plan for your health and hard earned dollars!

0 Comments

New Illinois Medicare Supplement Annual Open Enrollment Period: No Health Questions Required!Starting January 1, 2022, if you are a resident of Illinois and are between the ages of 65 and 75, you may have a new annual open enrollment period when you can change your Medicare Supplement coverage without having to answer health questions. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

The new Illinois Medicare Supplement Annual Open Enrollment Period is called the Birthday Rule: https://trackbill.com/bill/illinois-senate-bill-147-ins-medicare-open-enrollment/2023061/

Here’s how it works: You have to live in Illinois. You have to be between age 65 and age 75. If you meet both of those qualifications, you may have a Medicare Supplement open enrollment period every year that lasts 45 days with the first day being your birthday. During that time you can change your Medigap coverage with no underwriting and no health questions. Restrictions There are some restrictions on the changes your are allowed to make. 1. You have to move from higher coverage to lesser coverage. So if you have a Medicare Supplement Plan F, you can move to a G, an N, any plan with less coverage than F. Same for G, N, and any other Medicare Supplement. If you have a High Deductible Plan G, there isn’t any plan with less coverage, so this open enrollment wouldn’t be able to be used. You can’t move from less coverage to more coverage. So if you have a high deductible F or G or a Medigap Plan N, for example, you can’t purchase a standard G, without having to go through underwriting with health questions. 2. You have to stay with the same insurance company. This open enrollment period does not allow you to change Medicare Supplement companies. Only to change plans within the same company. This is an important restriction. If you purchased your current Medigap plan from a subsidiary company of a very large insurer, and that subsidiary is no longer accepting new Medicare Supplement applications in Illinois, then you can’t use this open enrollment period. If you qualify, your current Medigap company will notify you at least 30 days before your open enrollment period begins. What will this new law do to Medicare Supplement rates? In other states with broad Medigap open enrollment periods, rates for most Medicare Supplement policies are extremely expensive. It’s too soon to tell what will happen to IL rates. Because the IL Birthday Rule limits changes to moving from higher to lesser coverage and staying with the same insurance company, hopefully, this will not have an adverse effect on rates for everyone with a Medicare Supplement in IL. Have Questions? We Can Help! If you have questions about your Medicare Supplement coverage, or any other Medicare questions, please feel free to give our office a call at 877-312-1414 or schedule a free, no obligation Medicare Plan Consultation. We’re here to keep you up to date on your Medicare options, so you can find the best plan for your unique situation. Medicare Part D for People Who Take No (or Few) MedicationsMedicare Part D is the part of Medicare that covers prescription drugs. Part D plans are not offered by Medicare itself. Rather, Medicare authorizes Part D plans from private insurance companies that meet yearly standards set by Medicare to be sold to the public. If you take expensive prescription medications, it’s definitely to your benefit to enroll in a Part D plan when you become eligible for Medicare. But what if you take only a few inexpensive generic medications or no medications at all? Should you enroll in a Part D plan? Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

Part D Enrollment

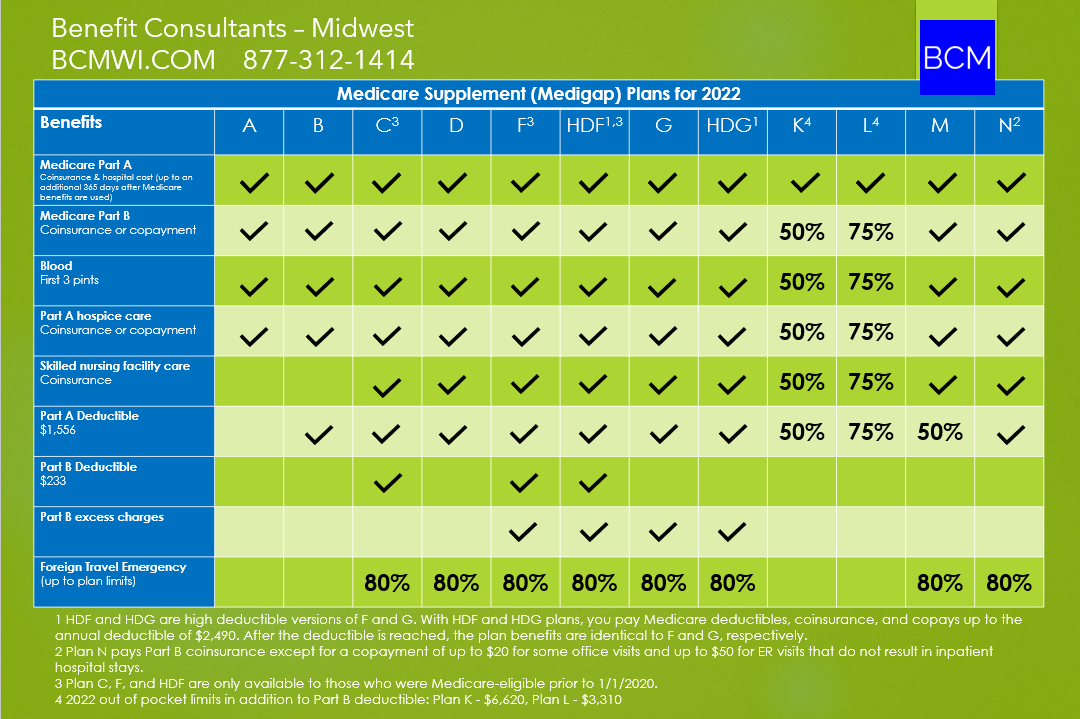

Part D enrollment is not required by Medicare. However, enrollment in Part D is incentivized by Medicare. With any insurance product, the goal is to have as many people as possible in a group to spread financial risk around. That’s why, when Medicare Part D was set up about 15 years ago, a hefty late enrollment penalty was included to strongly encourage everyone eligible to enroll in a Part D plan, even those who take few or no medications. Initial Enrollment Period (IEP) Most people first become eligible for Medicare when they turn 65. The first opportunity to enroll in a Part D plan is your Initial Enrollment Period (IEP): if you are enrolling in a Medicare Part D plan when you turn 65 and are enrolling in Medicare Parts A and/or B, your IEP is the three months prior to your birth month, your birth month, and the three months following your birth month, for a total of seven months. It's important to make a note of those seven months because you aren’t able to enroll in a Medicare Part D plan anytime you might want to during the year. If you choose not to enroll during your Initial Enrollment Period, your next chance to enroll, unless you have something that triggers a Special Election Period, will be the Annual Enrollment Period between October 15 and December 7. Any enrollment completed during the Annual Enrollment Period takes effect on January 1 of the following year. Late Enrollment Penalty If you don’t enroll in Part D coverage during the seven months of your Initial Enrollment Period, and you don’t have creditable prescription coverage from another source like a group health plan from your employer or union or a government program such as the VA, your Part D late enrollment penalty kicks in. The cost of the late enrollment penalty depends on how long you didn’t have creditable prescription drug coverage. The late enrollment penalty is calculated by multiplying 1% of the “national base beneficiary premium” ($33.06 in 2021, $33.37 in 2022) by the number of full, uncovered months that you were eligible but didn’t enroll in Medicare drug coverage and went without other creditable prescription drug coverage. The final amount is rounded to the nearest $.10 and added to your monthly premium. Since the “national base beneficiary premium” may increase each year, the penalty amount may also increase each year. After you enroll in Medicare drug coverage, the plan will tell you if you owe a penalty and what your premium will be with that penalty added. Penalty Examples So, for example, if your seven months of Initial Enrollment Period end March 30, 2022, and you don’t enroll in Part D coverage and don’t have creditable coverage from another source, the earliest you can enroll in a Part D plan is the next year, 2023, on Jan 1. The intervening 9 months without coverage are all subject to the late enrollment penalty. In 2022, that’s 30 cents per month for each month not enrolled in a Part D plan or creditable coverage, which adds up to an extra $2.70 per month that gets added to your Part D plan premium when you enroll. An extra $2.70 a month doesn’t sound too bad. However, remember though that the penalty amount is always calculated using the national base beneficiary premium for the year, and that almost always goes up, so your penalty amount will increase every year. Also, the big issue is that you will pay an extra $2.70 per month for as long as you are enrolled in Part D coverage. It never goes away. So, if our hypothetical person has Part D coverage for 20 years, and to keep the math simple, let’s assume the penalty stays at $2.70 a month for all twenty years, even though in the real world, that’s very unlikely. After 20 years, our person has paid an extra $648 in late enrollment penalty. Remember, that person only had 9 months of non-coverage. If you go for years without coverage, the penalty amount continues to grow. If someone didn’t have Part D coverage for 5 years and wants to enroll in a Part D plan for Jan 1, 2022, that person’s monthly late enrollment penalty would be an extra $18 tacked onto a Part D plan premium. If that person spends 20 years on a Part D plan, the total penalty paid would be $4,320. The longer a person doesn’t have Part D coverage, the worse the penalty gets. Ok, what are the alternatives? You can go without Part D coverage and plan to self-fund all prescription costs. We’ve had a few clients over the years who have chosen to do this and have the financial reserves to make that possible, but for most people, this is a risky option. Medications for some medical diagnoses are extremely expensive and can eat through retirement savings quickly. None of us knows what our health future holds, but for most people, as we age, we need more medical intervention, including more medications. The course of action we recommend is to enroll in the Part D plan with the lowest monthly premium in your zip code during your Initial Enrollment Period if you take no medications. The insurance companies know that there are a growing number of people who are in their 60s and don’t need maintenance medications. There are usually at least a few plans in every zip code with very low premiums. For 2022, there are plans that have premiums of less than $10 per month. If you take no medications and enroll in a $10 per month Part D plan for all of 2022, that’s a total of $120 spent to avoid the late enrollment penalty later. Enrolling does also give you, obviously, Part D prescription drug coverage. If you have illnesses or injuries during the year, you have coverage for any medications your doctor may prescribe. Have Questions? We Can Help! If you have questions about Medicare Part D prescription drug coverage, or any other Medicare questions, please feel free to give our office a call at 877-312-1414 or schedule a free, no obligation Medicare Plan Consultation. We’re here to help you understand your Medicare coverage options and choose the plan that’s the best fit for you. 2022 Medicare Supplements Chart

Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

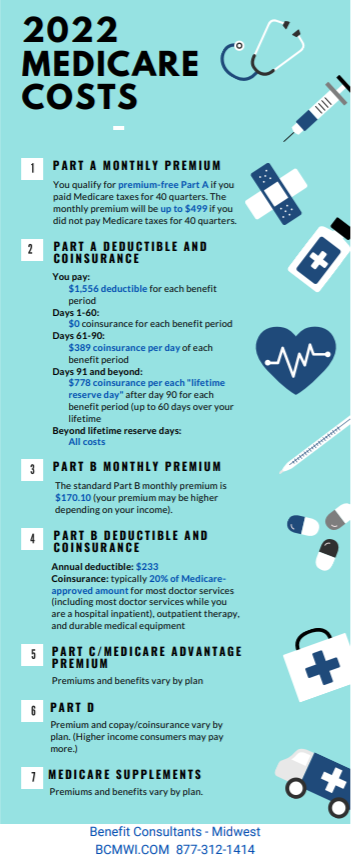

2022 Medicare Costs at a Glance

At A Glance: 2022 Medicare Costs

Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

Enroll in a Medicare Advantage Plan Dec 8 - Nov 30 with the Five Star SEP!

Once the Annual Enrollment Period (Oct 15 - Dec 7) has passed, what options do you have for Medicare Advantage enrollment the rest of the year?

In many cases, you are locked into your chosen Medicare Advantage plan for the calendar year, but there are exceptions. Options vary depending on what plans are available in your zip code and your circumstances throughout the year. Different events in your life can trigger a Special Enrollment Period or SEP. In this video, we’re going to look at a Special Enrollment Period option that doesn’t require any change in your life to qualify for: the Five Star Special Enrollment Period. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

What is the Five Star Special Enrollment Period?

Medicare uses information from member satisfaction surveys, plans, and health care providers to give overall performance star ratings to Medicare Advantage and Part D plans. A plan can get a rating between 1 and 5 stars. A 5-star rating is considered excellent. Medicare updates these ratings each fall for the following year. Plan ratings can and do change every year. All plans work toward earning a five star rating. Not only does a five star rating help inspire consumer confidence in a plan, it also gives the plan extra Special Enrollment Period rights to enroll new members. The Five Star Special Enrollment Period runs from December 8 through November 30. You are allowed to make one plan change during that time to enroll in a Five Star Medicare Advantage or standalone Part D Plan. Medicare Advantage plans overall have improved significantly in the past few years. That’s reflected in the star ratings. For 2021, only 21 plans had a 5 star rating. For 2022, the number of 5 star plans has gone up to 73. These plans are not evenly distributed across the country. There are some counties where there are over a dozen 5 star Medicare Advantage plans in 2022. Then, there are also some counties with no 5 star plan options. If you don’t have a 5 star plan in your zip code, you are not able to use the 5 star Special Enrollment Period. If you do have one or more 5 star plans in your county, you are able to use this Special Enrollment Period between December 8 and November 30. How can you use this Special Enrollment Period? You are eligible to use this SEP if you are already in a Medicare Advantage plan (either MA only or MAPD with drug coverage) or if you have coverage from Original Medicare and meet the Medicare Advantage eligibility requirements, which include being enrolled in both Medicare Parts A and B and living in the plan’s service area. If you choose to use the 5 star SEP, coverage will start the first day of the month after you apply. This option can only be used once between December 8 and November 30, so just like during other enrollment periods, look at the plan carefully to make sure it’s a good fit for you before enrolling. A five star plan that doesn’t have your doctors and hospitals in its network might not be something you want for your coverage, for example. Once the 5 star SEP is used, you are locked into that plan, unless your situation gives you some other Special Enrollment Period, until the next Annual Enrollment Period from October 15 through December 7. Part D Coverage Note Please note, if you move from a Medicare Advantage Plan that has drug coverage to a 5‑star Medicare Advantage Plan that doesn’t, you’ll have to wait until your next enrollment opportunity to get drug coverage, and you may have to pay a Part D late enrollment penalty. If you’d like to see if there are any 5 star Medicare Advantage plans in your county, please feel free to give our office a call at 877-312-1414 or schedule a free, no obligation Medicare Plan Consultation. We’re here to help you navigate the confusing world of Medicare to find the best coverage possible for you! Should I Keep the Same Insurance Company I Have Now Once I'm Eligible for Medicare?When you’re near Medicare eligibility, you get tons of mail from insurance companies. Including your current insurance company. Your current health insurance company will suggest that you transition from its plan that you’re currently on to its Medicare plan when you enroll in Medicare. The question is: is doing that in your best interest? Insurance companies want to keep your business. Every company wants to keep your business. When you enroll in Medicare, your options for health coverage become very different from what was available before you had Medicare, so in this video, we’ll go through how to evaluate whether staying with your current health insurance company after you’ve enrolled in Medicare is a good idea or not. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

Is your health insurance tied to other benefits?

The first thing to consider is whether your health insurance is tied to other benefits. If you are on group health insurance provided through an employer or union, this may be the case. If you purchase your own individual health insurance, it is almost certainly independent of any other benefits. For all those on group insurance, whether you are going to continue working past age 65 or you are going to retire, your benefits administrator will be able to tell you if you have to stay with your group health plan to keep other benefits, which may include other insurance or retiree and pensions plans. If disenrolling from your group health plan would cause you to lose other benefits, it probably isn’t a good idea. If your group health plan is not tied to other benefits, it’s worth your time to look at individual Medicare plan options. Again, this is true whether you are going to continue working once you are eligible for Medicare or you are retiring. How to Compare Group Insurance vs Individual Medicare Plans We put these comparisons together for our clients. There are several factors to consider: any monthly premium you pay for your group plan, whether the size of your group requires that you enroll in both Medicare Parts A and B when you turn 65 with the added premium cost of Part B if that’s necessary (more about that in the video here), and the benefits of your group plan with associated potential costs like deductibles, copays, and out-of-pocket maximums. All of that needs to be compared with the costs and benefits of Medicare plans available in your area. Any Medicare plan will also have that Part B monthly premium cost in addition to any plan costs, so that needs to be included on the Medicare side of the comparison. Because individual Medicare plans are completely different from group health insurance plans, the company you currently have for your group health insurance isn’t really relevant. The individual Medicare plans are regulated differently, to some extent run differently, may have different provider networks, and have no association with the group plans from the same company. So, although we always include any available individual Medicare plans from your current health insurance company in comparisons, there’s no benefit to you in staying with that company. Its Medicare plans have to compete for your business just like every other company’s plans. If You have Individual Coverage before Medicare Eligibility For all of you, whether you are on health insurance you purchase through the Marketplace, a short term plan, or you’re with a health cost sharing organization, when you turn 65, those options all go away. In your case, at age 65, you need to sign up for both Medicare Parts A and B, and you’ll be looking at individual Medicare plans. If you have insurance through the Marketplace or a short term health plan, and if your current company has Medicare plans in your area, I guarantee it will contact you many times to encourage you to just transition to one of that company’s Medicare coverage options. The question to ask is: is there any benefit to you in doing that? The answer is: no, there is not. Your individual health plan has no connection to the same company’s Medicare plans. There is no benefit to you to just aging into the same company’s individual Medicare plans. Actually, doing so without comparison shopping all Medicare plans open to you could cost you a lot more money than you need to spend. We get calls from people who stayed with the same company they had for individual under age 65 health insurance and after a few years on Medicare, they get around to looking more closely at the plan and find it really wasn’t a good fit for them. Unfortunately, by then, Medicare plan enrollment options are more limited for some plans than they were when people were just aging into Medicare. Like in every other circumstance, you need to be an educated consumer. Yes, Medicare is confusing. And, yes, it does take a little time to compare your options. But doing that at age 64 will save you so much hassle and money down the line. You don’t have to do it alone. Medicare plan brokers can explain to you how each type of Medicare plan works and comparison shop with you to find the plan that best fits your finances and healthcare needs. That might be a Medicare plan from your current health insurance company. Or it might be some other company. If you are turning 65 soon and have questions about your Medicare options, please feel free to give our office a call at 877-312-1414 or schedule a free, no obligation Medicare Plan Consultation. . We provide clear explanations and comparison shop all available plans with you, so you can be confident when you start your time on Medicare that you have the best possible coverage for you. |

How to Find the Best Medicare Coverage Without Paying More Than You Need To... Tabitha MoldenhauerLicensed health and life insurance broker since 2005 serving Alabama, Arizona, California, Colorado, Florida, Georgia, Idaho, Illinois, Indiana, Michigan, Minnesota, Missouri, North Carolina, New Hampshire, New Jersey, New Mexico, Nevada, Ohio, Tennessee, Texas, Utah, Virginia, Washington, and Wisconsin. Categories |

||||

RSS Feed

RSS Feed