When you start looking at Medicare options, it can seem overwhelming.

Don’t despair!

Today, we’re going to break down Medicare Supplements so you will know how to figure out which one is the best option for you if you choose a Medicare Supplement for your health coverage.

Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To…

What Are Medicare Supplements?

Medicare Supplements, also known as Medigap plans, are insurance policies that fill in the gaps that would otherwise be your out-of-pocket costs in Original Medicare, Parts A and B.

Medicare Parts A and B are your primary insurance coverage. If you have a covered medical expense, Medicare pays its responsibility first, then your Medicare Supplement pays based on the plan’s benefits.

Medicare Supplements are much older than Medicare Advantage Plans and Medicare Part D plans and have different rules and laws governing them.

Why would you choose a Medicare Supplement for your coverage?

If you have a Medicare Supplement, you don’t need to worry about provider networks because, if you have a standard Medicare Supplement, there are no networks. You can see any medical provider who accepts Medicare. This makes Medicare Supplements popular with people who don’t want their choice of doctors restricted by an insurance company.

You also don’t have to worry about benefit changes. Insurance companies can’t make any changes to Medicare Supplement benefits. These plans are standardized by law, so the only time benefits change is when a new law changes Medicare Supplements across all companies.

Also, there’s no need to take time to compare Medicare Supplements during the Annual Enrollment Period between October 15 and December 7 because Medicare Supplements are not affected at all by the Annual Enrollment Period. They are month to month contracts that you can change any time during the year.

The rules for changing Medicare Supplements do vary from state to state and can depend on your health and how long you’ve been on Medicare.

If you are beyond your first six months on Medicare Part B and don’t have a guaranteed issue right, you will have to answer health questions and go through underwriting to be able to purchase a new policy. For most people, that isn’t a barrier to changing. More information on Medicare Supplement underwriting can be found in the video linked here: https://youtu.be/br-4S0U912U.

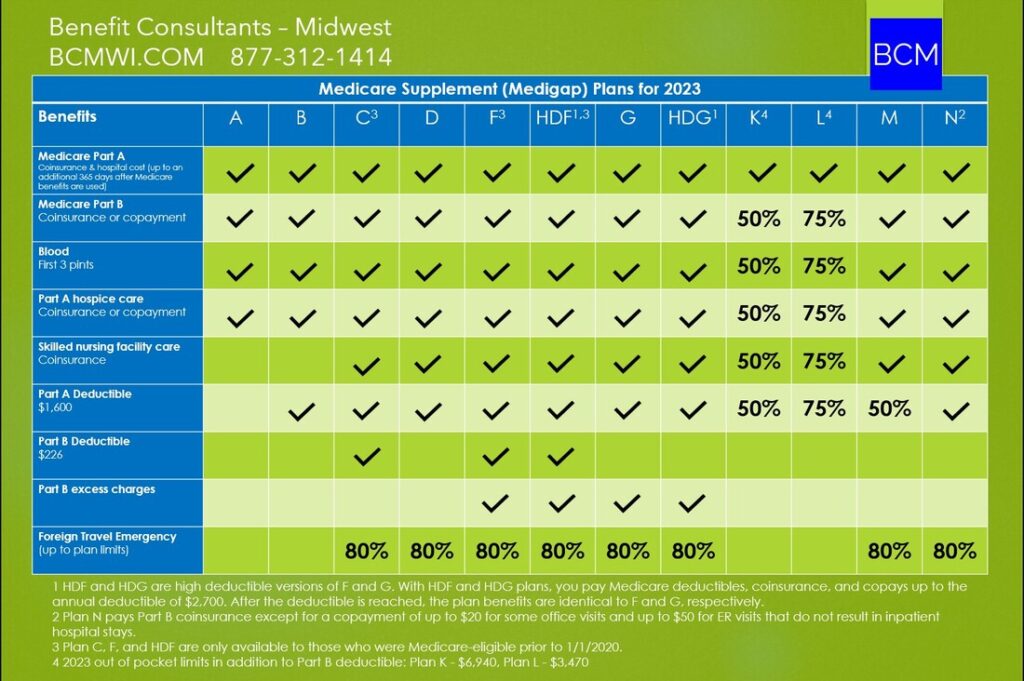

Medigap companies have to offer Plan A, and beyond that, each company chooses which other plans (B, C, D, F, HDF, G, HDG, K, L, M, N) to market in each state.

Some of the plan designs don’t make much sense financially for Medicare beneficiaries, so very few insurance companies even offer them. That’s the case with B, D, K, L, and M. Also, Plans F and C are only options for people whose Medicare Parts A and B effective dates are before Jan 1, 2020.

Even if you have been on Medicare long enough to be eligible to purchase a Plan F, it’s not a good idea. More on why that is in the video linked here: https://youtu.be/M81-iDbIfpo.

After those eliminations, the plans that offer the best value for consumers are Plan G, Plan N, and High Deductible Plan G.

Let’s look at each of these in detail.

Medigap Plan G

Plan G is the most comprehensive Medigap plan of the three. For all medical care covered by Medicare Parts A and B, your out-of-pocket risk with a Plan G is limited to the Part B outpatient annual deductible. In 2023, this deductible is $226.

If you reach that deductible, all outpatient expenses beyond that are covered between Medicare Part B and Plan G at no cost to you. This includes things like office visits, diagnostic testing, and all outpatient treatment.

On the inpatient side, all covered expenses are split between Medicare Part A and Medigap Plan G. You have no out-of-pocket deductible for inpatient care.

Because Plan G has the most coverage with the least risk of out-of-pocket spending for you, it is the most expensive of these three Medicare Supplement options.

Since Medicare Supplement prices generally go up once a year as you age, we need to think about future costs in addition to the initial price when you first apply.

Plan G is more expensive when you first enroll, and you can expect yearly increases in the premium to be larger than what a Plan N or High Deductible Plan G will have.

Who should consider Plan G?

If you have very expensive, ongoing treatments like chemotherapy, treatment for rheumatoid arthritis, or any other medical condition that needs regular or costly care, a Plan G can be a good choice for you.

That higher Plan G monthly premium is balanced out by the savings in out-of-pocket costs because you don’t have a big deductible to meet or any copays.

High Deductible Plan G

At the opposite end of the coverage spectrum, we have High Deductible Plan G. This Medicare Supplement provides exactly the same coverage as Plan G, with one big difference: You have to meet a high deductible before the High Deductible Plan G will pay anything.

In 2023, that deductible is $2,700. If you have a High Deductible Plan G, you pay the Medicare Part A and B inpatient and outpatient deductibles, copays, and coinsurance up to $2,700. If you reach that amount in your spending, then the Medicare Supplement kicks in and pays just like a standard Plan G.

Because this plan has the least amount of coverage and the biggest out-of-pocket risk for you, it has the lowest monthly premium cost. High Deductible Plan G also has the smallest premium increases every year.

Who’s an ideal candidate for a High Deductible Plan G?

If you are healthy and don’t need much medical care, this can be a great way to protect yourself from catastrophic medical charges while saving a ton of money on monthly Medicare Supplement premium costs.

In many parts of the country the difference in the premium between a Plan G and a High Deductible Plan G is well over $100 per month.

High Deductible Plan G rates also increase much more slowly than Plan G or Plan N rates.

Why not just have Original Medicare Parts A and B? Do I need a Medicare Supplement?

Medicare Parts A and B have no out-of-pocket spending limit for beneficiaries.

If you only have Medicare Parts A and B, there’s no limit to how much you can spend for your medical treatment in a calendar year.

A High Deductible Plan G provides a cap on what you can spend in a year, and if you have a serious illness or injury, you have the assurance that your spending, in addition to monthly premium costs, won’t exceed $2,700 for the year.

Medigap Plan N

Then, in the middle of the coverage options, we have Medigap Plan N. This is a newer Medicare Supplement plan, and it grows in popularity every year. It is like G but slightly less comprehensive.

Because Plan N has middle of the road coverage between Plan G and High Deductible Plan G, it also has middle of the road premium costs.

There are two differences between G and N. Both are in the outpatient coverage. Inpatient coverage is identical between plans G and N.

Medicare Part B Excess Charges

One difference is that Medicare Part B Excess Charges are not covered by Plan N. In most cases, that’s not a big concern.

The only time you can be billed an excess charge is if you see a doctor who contracts with Medicare as a non-participating provider. Only about 4% of Medicare providers contract with Medicare as non-participating providers.

A non-participating provider accepts Medicare patients but doesn’t accept Medicare payments as payment in full and can balance bill patients up to 15% more as an excess charge.

To find out how your providers are contracted with Medicare, you can use the Physician Compare tool at medicare.gov.

Of course, the easiest way to avoid excess charges is to only use providers who contract with Medicare as participating providers.

If you must use a non-participating Medicare provider, how often can you expect excess charges to show up on your bill?

A few years ago, one of our Medicare Supplement insurance companies looked at all their claims for one year and found that 99.34% of claims had no excess charges. Of the 0.66% of claims that did include excess charges, the average cost of an excess charge was under $20.

Excess charges are rare, and they aren’t automatic if you are seeing a non-participating provider. The provider can decide whether to balance bill a patient on a case by case basis, and the amount is not always an extra 15%. The rule is the excess charge can be up to 15%, so it may be less.

The risk of excess charges is so low that paying extra for a Medigap plan that covers excess charges generally doesn’t make much sense.

Outpatient Copays

The other difference between G and N is that with Plan N, after meeting your Part B outpatient deductible for the year, you may have copays for office visits of up to $20 and for ER visits of up to $50, although that’s waived if you are admitted to the hospital.

These office visit copays are not charged at every visit. It depends on how your visit is coded by your provider’s office. So, it isn’t guaranteed that you will have any copay at an office visit, but if you do, it is capped at $20.

How to Choose Between Medicare Supplement Plan G and Plan N

If you’re trying to decide between a Plan G and a Plan N, look at the difference in the premium cost between the two plans in your zip code and estimate how many office visit copays you are likely to pay in a year.

Premiums vary widely from one state to another.

Here are a couple quick examples from rates in Illinois.

For a male, age 70, a Plan N has a premium savings of about $35 per month over a Plan G, for a total of $420 per year.

If he makes fewer than twenty office visits per year, the Plan N is the better value.

For a female, age 70, Plan N saves about $30 per month versus Plan G, for an annual savings of $360.

If she makes fewer than eighteen office visits per year, Plan N is the better financial value.

Remember, there are also future costs to consider when choosing a Medicare Supplement. Because Plan N has slightly more out-of-pocket risk for policy holders, the rates increase more slowly than Plan G premiums.

Comparison Shopping Medicare Supplements

Once you’ve decided on the Medicare Supplement Plan that has the right level of coverage for you, it’s time to comparison shop all the companies that offer that plan in your area.

Although the coverage is standardized by law, the costs from company to company for the exact same plan are wildly different.

Different companies use different pricing models, so it is really important to do detailed comparison shopping and research before applying. It can save you a lot of money initially and in future years.

This is what we do for all of our clients as Medicare plan brokers. We work with many insurance companies and can impartially comparison shop with you to find the plan and the company that’s the best fit for your situation.

We do this completely free of charge to our clients. We’re able to do that because for every enrollment into a Medicare plan through our office, we are paid a commission by an insurance company.

The commissions are similar across plans and insurance companies, so we have no reason to push one company over another for our own gain. We are free to find the plan and the company that fits each client’s medical and financial situation best.

The Medicare plan cost to you is the same whether you buy direct from an insurance company or purchase through a Medicare plan broker.

Once you are a client of ours, you have ongoing free access to expert help whenever you have a question about your coverage or when premiums or plans change and you need to re-evaluate and possibly switch Medicare Supplement policies.

If you have Medicare Supplement questions, please feel free to give our office a call at 877-312-1414 or schedule a free, no obligation Medicare Plan Consultation.

We’re here to help you understand your options and find the best Medicare plan for you!

Leave a Reply