Today we’re taking a look at Medicare Supplement Plan G versus Medicare Supplement Plan N. Which makes more sense or is more cost effective in your situation?

Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To…

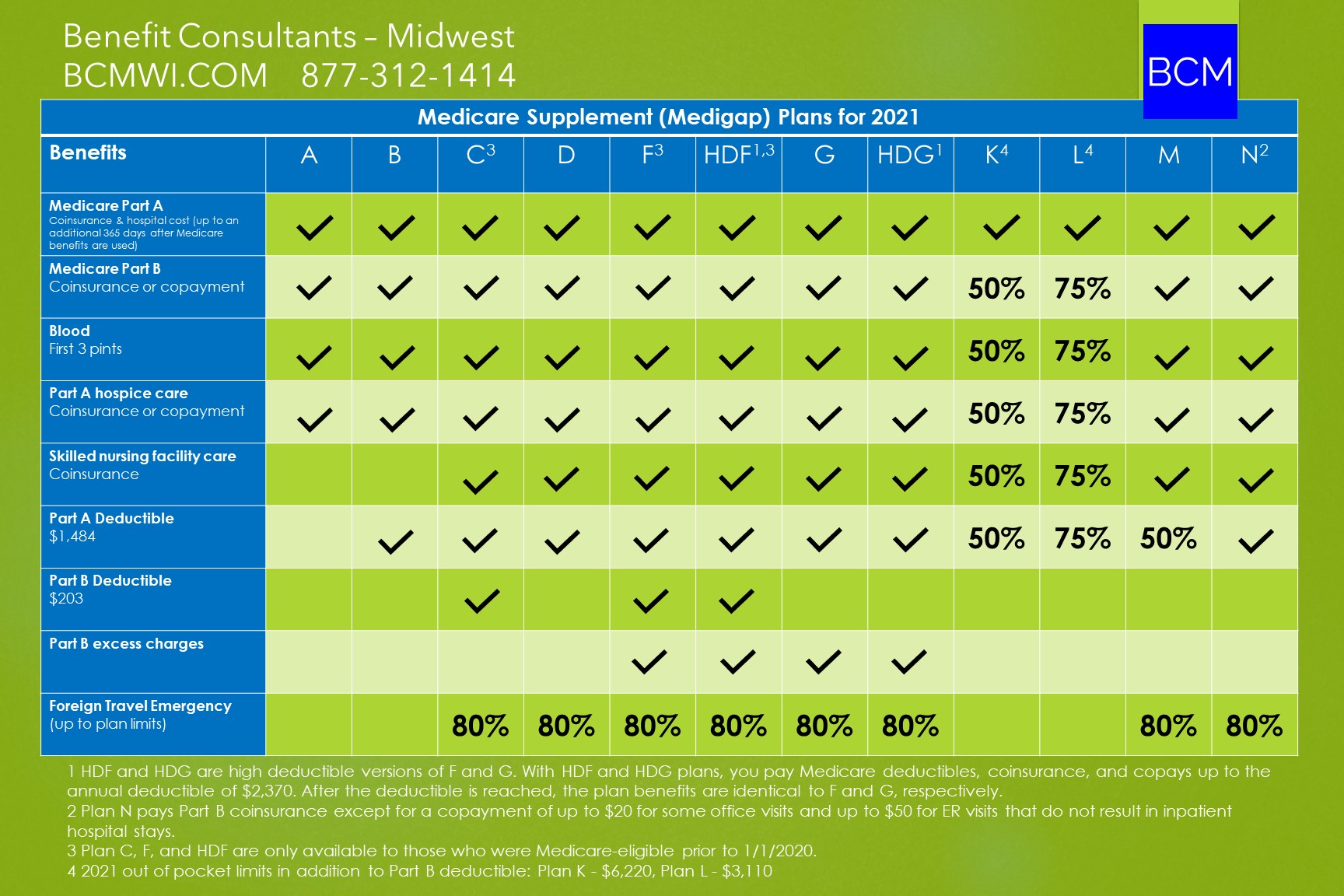

Here we have a chart of the standardized Medicare Supplement plans as they are sold in 47 states. Illinois and Indiana have these plans. Wisconsin has a different version of standardized plans.

Comparison of Benefits

Let’s take a quick look at the benefits.

Even though they aren’t at the top of the chart we’re going to start with the deductibles because those are the first things that you would be responsible to pay.

Part A deductible of $1,484

This is your inpatient or hospital deductible, and this deductible is charged for each benefit period. A benefit period starts the day you are admitted as an inpatient and ends after you’ve had 60 days in a row without inpatient or skilled nursing facility care.

An important thing to remember is you can end up being charged this deductible more than once in a calendar year.

Part B deductible of $203

Underneath that we have the Medicare Part B deductible. This is your outpatient care. It’s an annual deductible, so once you pay that $203 in deductible charges for the year, you are done for that calendar year.

Coinsurance and Copayments

Once your deductibles are met, then you have coinsurance and copayment amounts. Generally, Medicare pays about 80 percent leaving about 20 percent as your responsibility.

Blood Transfusions

Then, underneath that, if you need a blood transfusion, Medicare does not cover the first three pints of blood, so that would be your responsibility.

Hospice Care

Next on the chart: hospice care coinsurance or copayments. Those are generally quite minimal. Medicare does a nice job of comprehensively covering hospice care.

Skilled Nursing Facility Care

Then we have the skilled nursing facility care coinsurance. Medicare only covers skilled nursing facility care after a three-day inpatient hospital stay, and only for 100 days. Custodial care in a skilled nursing facility is not covered by Medicare at all.

The coinsurance listed here is a per day charge of $185.50 for each of the days 21 through 100. This works on the benefit period schedule just like a hospital stay, so it’s possible to have more than one benefit period per year.

Medicare Part B Excess Charges

Under that then we have, down under the deductibles, Medicare Part B Excess Charges. I have another video devoted to Excess Charges. You don’t really need to be concerned about Excess Charges. If you want the details on why please see the other video.

Foreign Travel

Then, foreign travel. This provides some emergency care internationally, but I still recommend that everyone traveling out of the country purchase travel medical insurance.

Medicare Supplement Plan G or Plan N

If you turned 65 after January 1st, 2020, Plan G is the most comprehensive Medicare Supplement plan that you are allowed to purchase. It’s a very good plan. I have lots of clients with a Plan G, and they’ve been very happy with it.

Plan N is newer. It came out in 2010 and has been gaining in popularity ever since it was released. There are two differences between Plan G and Plan N. Both are in the outpatient side of coverage. The inpatient, Medicare Part A, benefits are absolutely identical.

Outpatient Differences Between G and N

The difference you can see on the chart is that Plan G covers Medicare Part B Excess Charges and Plan N does not. As mentioned earlier, that’s not really a big concern. If you’d like more information on the Excess Charges, again, please see the other video.

The other difference is that with Medicare Supplement Plan N, after you meet your Medicare Part B outpatient deductible for the year, you may have co-pays for office visits of up to $20 per visit, and for ER visits of up to $50 per visit, although the ER visit copay is waived if you end up being admitted as an inpatient.

How to Compare G and N Potential Costs

To compare G and N, we look at the difference in the premium between the two plans for your zip code and your age, and we also need to look at how many office visits you are likely to make in a calendar year.

I have a few examples here. This is not from any particular carrier. This is an average of several different Medicare Supplement carriers, and this is what I found in the greater Chicago area, so Illinois and a little bit into Northwest Indiana too.

For a male, age 70, a Plan N saves about $35 a month versus a Plan G for an annual premium savings of $420. So if you are going to be making fewer than 20 or 21 office visits per year, the Plan N is probably going to overall save you some money. If you make more than 20-21 office visits per year then the Plan N, because you’re paying out so much in co-pays, might not actually save you that much money.

Because male and female rates are usually different, I also quoted female rates in the same area, the greater Chicago metro area. For a female ,age 70, the Plan N saves around $30 a month versus a Plan G for an annual premium savings of around $360. So the same sort of copay math applies: if you are going to be making fewer than 18 office visits a year, then the Plan N definitely would be the better deal. If you end up making more than 18 office visits per year, well then, maybe the savings aren’t so great, and you might want to look at a Plan G instead.

Rate Increases

One other thing to consider when you’re comparing these two is rate increases. Medicare Supplement rates generally increase once a year, and it’s impossible to 100 percent accurately predict what a rate increase is going to be because they’re based on how much the insurer paid out in claims in a region.

However, for the last decade, Plan N rates have had smaller increases year over year than Plan G has, and that’s expected to continue.

If you have a Plan G and would like to look at Plan N rates in your area for your age, or if you are new to Medicare and would like to look at all the options available to you, please feel free to contact us by phone at 877-312-1414, or by email, or watch our free online video to learn how to find the best Medicare coverage for you.

We’d be happy to go through your options with you and help you find a plan that best fits your needs in your specific circumstances.

{kind=link}

Leave a Reply